Robert M. Cutler

The Canadian market primarily comprises banking, long-respectable Canadian energy stocks (oil and gas), minerals, and a few other industries. The Canadian stock market has been volatile in recent months, as investors grapple with a number of factors, including rising interest rates, inflation, and the ongoing war in Ukraine. This article will discuss banking and energy.

In general, Canadian markets have not had impressive performance recently. However, new opportunities are appearing. Oddly, while September and October typically see a pullback in the markets, September has been good so far in Canada. There still appears to be a lot of cash on the sidelines.

Canadian Banking Concerns

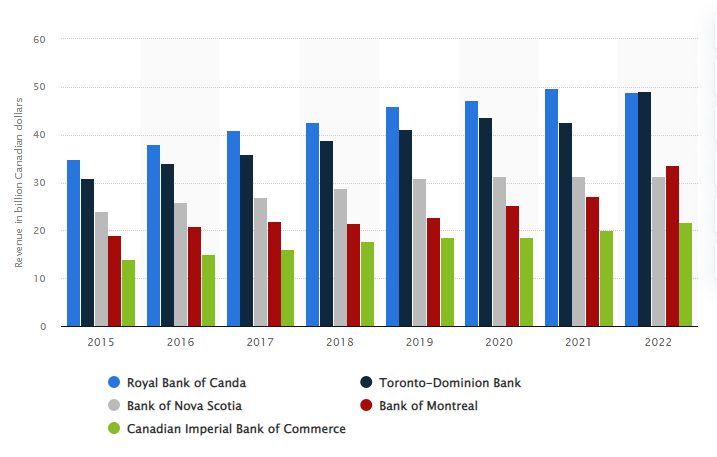

Let us start this review with the banking sector. At the present time, Canadian banks do not generate as much excitement among some investors. These banks have seen their stock prices approach 52-week lows. Compared to many U.S. banks, Canadian banks operate with a conservative approach. A looming concern is the state of mortgage rates in the country. Many homeowners with 3 to 5-year mortgages might face difficulties with interest rates, leading to potential payment defaults.

To mitigate this, some banks—particularly including major names such as Bank of Montreal (BMO), Toronto–Dominion Bank (TD), and Canadian Imperial Bank of Commerce (CIBC)—have offered rate options and longer amortization periods. However, such a strategy may not be sustainable in the longer term. It is worth mentioning, additionally, Canada has seen increased demand for rentals and homes due to rising immigration.

Over the past couple of years, those invested in Canadian bank stocks might have experienced losses. Despite the unattractive performance charts, the high dividends could be appealing for long-term investors, especially when compared to U.S. banks.

Is it time to get in now? The charts do not look very nice but the divideds are good. Perhaps when dividends get higher, these banks will be good buys for the long-term investor. They are very solid, compared to banks in the U.S. sector.

Challenges for Candian Energy Stocks

The Canadian energy sector has seen significant changes in recent years. Many American investors have sold their stakes in Canadian energy stocks, leading Canadian companies to acquire these assets. Under Liberal Party prime minister Justin Trudeau (and his minister of environment and climate change Stephen Guilbeault. a former Greenpeace Canada and Greenpeace International climate-change campaign organizer), Canada is focusing more on “green energy” solutions.

That means things like the development of battery-manufacturing plants. Quebec, with its abundant hydroelectric power, plays a central role in these plans. The problem is that the transition to a green economy will not happen anytime soon. The ruling party’s policies have had the result of neglecting Alberta’s resources, whether oil sands or regular oil and gas.

Nevertheless, key regions in Alberta such as the Peace River and Montney formations, host companies like Whitecap Resources, Crescent Point Energy, and Camerich Energy. These companies have been producing oil and gas very efficiently, with some wells recovering their costs in just six months. As the American companies reduced their involvement, Canadian firms stepped in.

Many of these Canadian energy stocks would be considered small in the U.S. context, but with their cashflows, and with current oil and gas prices where they are right now, they are positioned to finish paying back their debts in the next one to two years.

In the recent past, Canadian energy companies often spent more than they earned, focusing on aggressive growth. In this, they were like many U.S. companies following a “drill baby drill, grow at all costs” philosophy that was not necessarily the most fiscally responsible strategy. They sometimes relied heavily on banks for financial sustenance.

Today’s approach is different. These companies offer good dividends. Things have changed from the royalty-trust structure where they paid out everything. Now, while still offering dividends, these companies prioritize reducing their debts. Despite challenges like wildfires affecting operations, projections for upcoming production are positive. There is nevertheless a notable lack of support from the Canadian federal government for these endeavors.

Prospects for Canadian Energy Stocks

Despite these challenges, Canadian energy stocks are poised for growth. An important aspect for investors to consider is the cyclical nature of the oil and gas sector. Historically, there are periods where the sector doesn’t perform optimally. Currently, with oil prices where they are, this might be one of those downtrends. Yet, as these companies begin to release their financial figures, it could prompt investors to re-evaluate and potentially show renewed interest in the sector.

In terms of investing, Canadian energy stocks present a compelling case. They promise substantial returns and have a proven record of generating strong cash flows. However, the sector has been marred by a lack of interest, especially when it comes to mergers and acquisitions. Major players from the U.S. remain wary. Much of their skepticism stems from the present Canadian government’s stance on oil and gas resources.

As for pipeline companies, they are—like Enbridge for example—recovering from their 52-week lows. Interestingly, Enbridge recently secured funds amounting to $4–5 billion, with 80 percent backed by institutions. Despite offering a dividend yield of over 7 percent, from an investment standpoint, they have not been profitable in recent years.

Canadian Market Outlook

Canada’s benchmark stock index, the S&P/TSX Composite Index, has shown interesting behavior when compared to the Indian BSE Sensex Index, which I recently discussed. Whether denominated in Canadian dollars or converted into U.S. dollars, the recent TSX pattern resembles the Sensex U.S. dollar–denominated pattern.

It can easily be seen how the TSX followed an ascending channel from 2011 through 2020, until the chaos of the government-imposed economic lockdowns and resultant quantitative easing wrought havoc, pushing it to rebound above that channel (just like India’s Sensex) until it established a resistance level that now represents one leg of an ascending triangle.

Will the TSX pop out of that triangle to the upside? More detailed analysis would be necessary to answer this question. It should be noted that the TSX could actually pop out of that triangle to upside (or to the downside), and still regain its long-term ascending channel. The problem for investors is that the lower bound of that channel is about 25 percent below the current level, although there is decent technical support in the 17,500–18,000 range.

When evaluated in U.S. dollars, the TSX is even more interesting:

This chart shows a long-term (more or less) symmetrical triangle starting in 2008 that was violated to the downside by the market reaction to the economic shutdowns, and then to the upside by the government policies introduced to try to fix the problems that it had caused with the shutdowns. Again in the U.S. dollar–denominated chart, as in the Canadian dollar–denominated chart, the TSX has established a resistance level and is now in an ascending triangle.

The vertex of the U.S. dollar–denominated TSX ascending triangle will arrive, however, well before the vertex of the Canadian dollar–denominated TSX. We may be already in the critical period for this. The exchange rate will, of course, affect risk analysis for non–Canadian dollar investors. Further consideration of the issue, however, requires in-depth treatment of U.S.–Canada exchange rates, which will be the topic of a later subscription-only post.